The Student Loan Debt and Housing Report 2017 by the National Association of Realtors and the nonprofit group American Student Assistance shows the obvious: Student debt delays household formation, home buying, and saving.

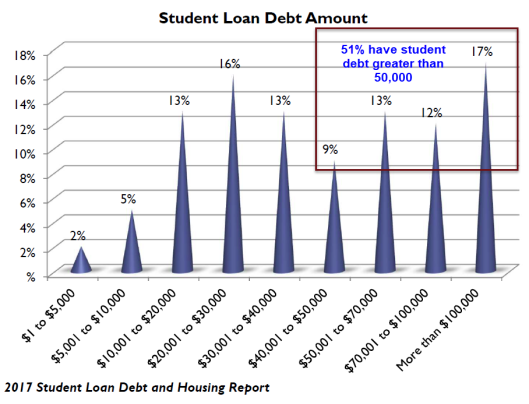

The U.S. currently has a student debt load of $1.4 trillion, which accounts for 10 percent of all outstanding debt and 35 percent of non-housing debt. The magnitude of the debt continues to grow in size and share of the overall debt in the economy. While this amount of debt has risen, the homeownership rate has fallen, and fallen more steeply among younger generations.

Student loan debt impacts other life decisions including employment, the state the debt holder lives in, life choices such as continuing education, starting a family, and retirement.

Twenty-two percent were delayed by at least two years in moving out of a family member’s home after college due to their student loans.

Among non-homeowners, 83 percent cite student loan debt as the factor delaying them from buying a home. This is most frequently the case due to the fact that the borrowers cannot save for a downpayment because of their student debt. Among homeowners, 28 percent say student debt is impacting the ability to sell their existing home and move to a different home. The delay in buying a home among non-homeowners is seven years and three years for homeowners.

More

8 comments:

Then don't go to college you can't have it both ways.

If the spoiled brats didn't have to have everything that comes down the pike instantly, maybe their debt wouldn't be beyond what they can afford.

After the student loan comes the luxury car lease. Has anyone noticed what these kids drive these days?

Some college kids use the government school loans for weddings vacations. Now they don't want to pay it back.

Let me clue both of you clowns in.

My fam grew up paycheck to paycheck. I had to take on loans to pay for school, despite having great grades. Despite going to a school that was ranked best in the region for value (cost per credit vs educational value) I still racked up debt so I could gain a degree in a leading science field (molecular biology/biotech). Well, in a field where you are calculating more than 2+2, you also need and advanced degree, hence more debt. You can't pay for school working through the type of jobs that are offered to folks who don't have a college degree these days. Not unless you plan to complete school at 45 yr old. Now that I am out of school, with a great job, earning good money, and providing quite a positive impact to society through my research, I still am paying off debt which delays my ability to purchase a home. This only further delays my ability to give fully back to the economy through my home purchase, property taxes, purchases of all the goods and services needed to build and maintain a home, etc. This is all because people your age created a world where you have to have a college degree to get a good-paying job and unless your parents were rich, you have to take on debt to get the degree. Is the picture a little less murky for you now?

BS 5:03

Not all great careers start with college degrees.

"Not all" correct. But please take 2 seconds to peruse the readily available economic data on lifetime income vs education level before you spew the rotten contents of your simple mind again.

Very well said 5:03 ! I Agree 100% ! ...Thanks For The Brekd

Post a Comment